Next Generation Satellite Systems Continue to Disrupt Satellite Capacity Pricing Landscape

Paris, France, February 12, 2024 - Euroconsult,has released the latest edition of its FSS Capacity Pricing Trends report which unveils continued shifts in the capacity pricing landscape.Satellite capacity pricing is experiencing rapid declines in an increasingly disruptive market, supported by rise of next-generation geostationary (GEO) and non-geostationary orbit (NGSO) high-throughput satellite (HTS) systems.

Massive influx of supply in the market has ultimately contributed to a commoditization effect on connectivity, due to which the industry is witnessing a shift towards managed service offerings with attractive $/GB economics, primarily driven by Starlink.

Satellite service pricing, driven by next-generation satellite systems, continues to re-shape the industry, triggering a transition towards managed services and attractive $/GB economics

Over the past five years, global average capacity pricing in video and data markets has dropped by approximately -16% (-3% CAGR) and -77%, (-26% CAGR) respectively. This decline is more pronounced in data markets due to abundant supply from NGSO (primarily Starlink) and HTS systems, while video markets have seen a lesser decline, largely due to stagnated regular supply and market stickiness to long-term contracted prices.

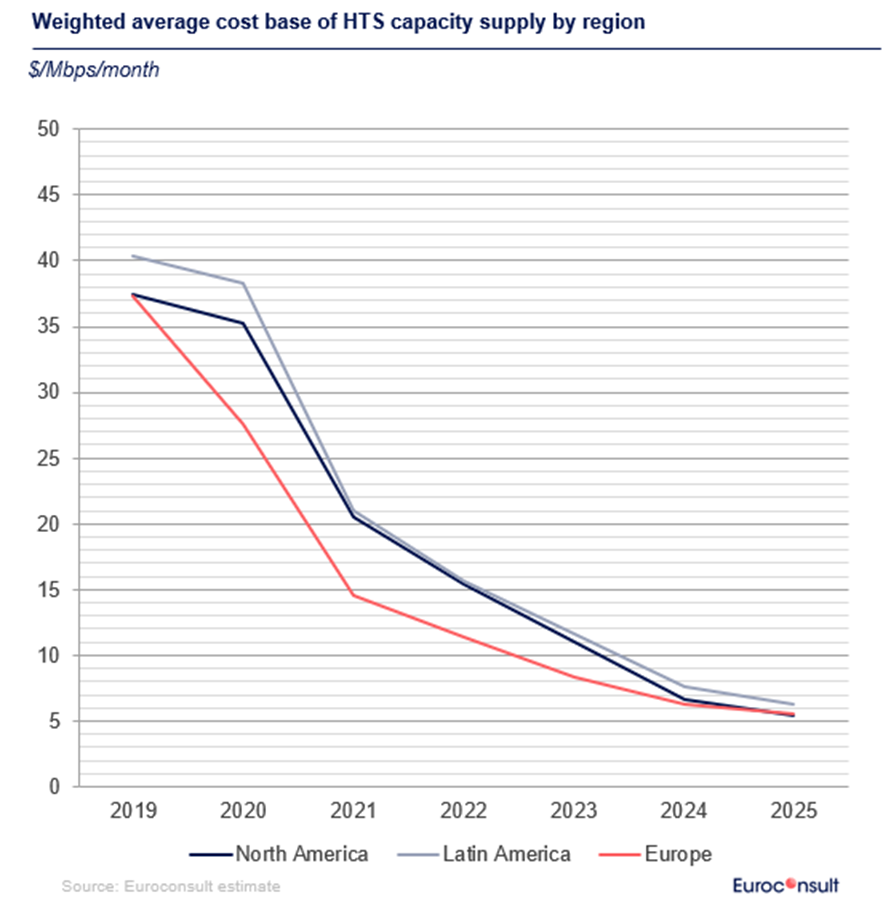

The report also notes that the decreasing cost base of capacity (indicating efficiency of capex invested in satellite manufacturing considering sellable capacity and expected lifetime), initiated with the advent of Starlink, is expected to stabilize over the next 2-3 years leading to a potentially slower capacity price erosion compared to previous years.

The dynamics outlined in the report signal continued changes for the industry, potentially marking a structural shift away from the traditional wholesale capacity leasing towards managed service packages supplemented by value-added services. This shift is triggering a re-alignment of operational strategies among industry stakeholders. Operators are moving towards vertical integration by providing managed capacity plans to service providers and/or directly to end users. Service providers are increasingly opting for these pre-made packages from satellite operators to reduce capacity management complexities and focus more on providing value-added services (Cyber security, Cloud connectivity, Telematics & IoT solutions etc.)

“Starlink's pocket-friendly pricing and higher availability of service plans have triggered a structural shift in the industry away from wholesale capacity leasing to more managed solutions setting a wave of strategy re-alignment across players. Operators are choosing to directly serve end customers with managed service plans giving them greater control of capacity prices while service providers are moving away from capacity management, focusing on value add-ons. ”, said Senior Consultant Grace Khanuja.

|

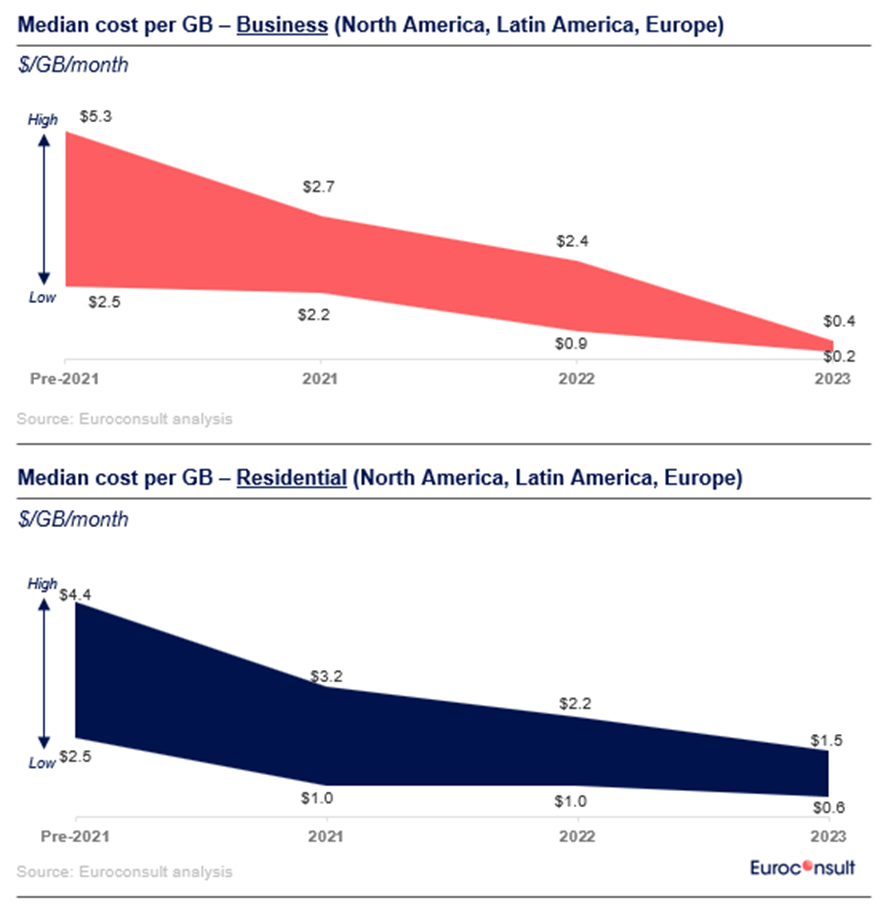

Owing to the shift in industry dynamics, the price per GB has witnessed a converging trend across key geographies over the past 3-4 years. The pre-2021 period was marked by median prices ranging greater than $2 to $5 per GB per month given the limited available capacity of legacy satellite systems that constrained monthly GB allowances. Rise in available capacity supply with the launch of Starlink across markets coupled with new service plans from incumbent satellite players (such as Viasat, Hughes in the Americas and Eutelsat Konnect in Europe) has abruptly lowered the price range to $0.2 to $1.5 per GB per month in 2023 given the disproportionate increase in GB allowances vs service plan costs.

The FSS Capacity Pricing Trends 6th edition is now available on Euroconsult’s digital platform in Standard and Premium versions, offering Euroconsult’s pioneering and unfettered data access and readability. A free extract can be downloaded.

About the Report

The FSS Capacity Pricing Trends report (6th edition) provides an assessment of the current dynamics for the pricing of satellite capacity in relation to sustained technology innovation and the additional satellite capacity associated with new generation satellites. The report (Classic version) includes 2023 capacity pricing benchmarks (reference and ranges as per primary/ secondary market research) and forecasts for the coming 24 months based on market/application and regional aspects. Historical price trends for capacity pricing in the last 3 years and a detailed service pricing database are included in the Premium version.

About Euroconsult

The Euroconsult Group is one of the leading global strategy consulting and market intelligence firm specialized in the space sector and satellite enabled verticals. Privately owned and fully independent, we have forty years of experience providing first-class strategic consulting, developing comprehensive market intelligence programs, organizing executive-level annual summits and training programs for the satellite industry. We accompany private companies and government entities in strategic decision making, providing end-to-end consulting services, from project strategy definition to implementation, bringing data-led perspectives on the most critical issues. We help our clients understand their business environment and provide them with the tools they need to make informed decisions and develop their business. The Euroconsult Group is trusted by 1,200 clients in over 60 countries and is headquartered in France, with offices in the U.S., Canada, Japan, Singapore, and Australia. www.euroconsult-ec.com.