by Hub Urlings

The satellite Internet of Things (SatIoT) market is expected to continue evolving rapidly in 2025. Incumbent operators continue to dominate, holding roughly 80% of market share by serving large corporations across defense, logistics, maritime, utilities and energy. Meanwhile, new entrants remain an essential source of innovation, seeking low-cost, low-power solutions to serve new markets, but struggle to scale their operations.

Despite the challenges faced by new entrants, growth prospects remain strong. Millions of active connections are already in place, and forecasts predict that adoption will accelerate through the next decade. This article examines the SatIoT market outlook, its role in the Fourth Industrial Revolution, sectoral adoption, competitive landscape, and the main topics shaping SatIoT’s trajectory toward 2030.

Market Growth and Forecasts

Estimates differ widely depending on definitions and scope. ABI Research projects 7.5 million active SatIoT connections by mid-2025, rising above 10 million by year-end and reaching 13.6 million by 2030. Other analysts are even more bullish, suggesting figures closer to 40 million connections.

These numbers are hard to verify. Are they only L/S band systems, or do they also include VHF, Ku, and Ka? Are telemetry backhaul links considered SatIoT? Should ADS-B aviation tracking count? Regardless of methodology, one thing is clear: SatIoT is expanding, with market research figures triggering hundreds of millions of investment dollars flowing into new constellations and enabling technologies.

Satellite IoT and the Fourth Industrial Revolution

The SatIoT market cannot be viewed in isolation. Its growth aligns with the broader Fourth Industrial Revolution (4IR), where sensors, edge computing, data analytics, automation, and ubiquitous connectivity are transforming industries.

Satellite IoT’s role is pivotal: extending data capture and communication into areas terrestrial networks cannot reach.

Like the development of 4IR, satellite IoT follows distinct phases: starting around 30 years ago with the emergence of the first satellite IoT applications e.g. in the defence sector and maritime, and followed by an early adoption phase for large corporations in energy and utilities, from 2020 onwards we are in scaling up phase with arrival of the next generation satellite IoT operators, and progressing to an eagerly awaited maturity phase around 2030 with cross industry adaptation and SME mainstreaming.

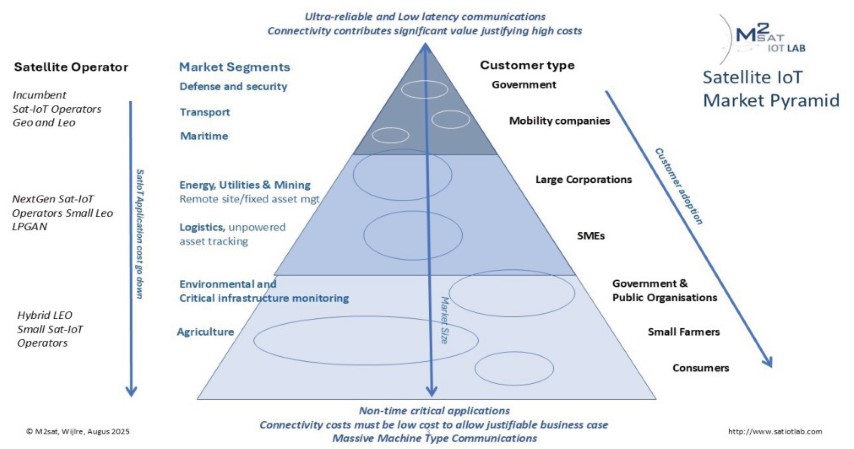

The Satellite IoT Market Pyramid

To describe the dynamics in the satellite IoT market dynamics we use a Pyramid model.

In the model, we can identify several trends on both the demand and supply sides.

Let’s start with the demand side.

"...ABI Research projects 7.5 million active Satellite IoT connections by mid-2025, rising above 10 million by year-end and reaching 13.6 million by 2030..."

Now in 2025, we see several established Market segments with strong growth:

- Defense & Security: Remote surveillance, asset tracking, border monitoring, and secure communications remain cornerstones. Goes through rapid growth at the moment.

- Transportation, Logistics and Automotive: Poised to become the largest segment by 2030, with applications in freight and container tracking, refrigerated cargo, and beyond-line-of-sight aircraft telemetry

- Maritime: Ship and cargo monitoring, offshore infrastructure connectivity, and climate data collection ensure maritime stays a top-three sector.

- Energy, Utilities & Mining: Real-time monitoring of pipelines, grids, rigs, and mines supports resilience and efficiency.

All existing segments show strong growth. Over the next decade, expanding demand is expected, particularly in the defence sector, as well as in transportation, automotive, logistics, and global supply chains.

The growth in these segments, however, cannot account for the full market size as forecasted by Market Analysts. For that, we need to examine emerging segments that will drive next-phase growth.

The real explosion in the coming 10 years is expected from new markets:

- Environmental Monitoring: Disaster response, flood and seismic monitoring, and air quality sensors are essential for climate adaptation strategies. By 2035, SatIoT will underpin global environmental data networks. Government investment in space and digital infrastructure is typically in two main sectors: defence and security, and environmental monitoring. Where the growth in the defence sector seems to be on a global scale, the approach to environmental monitoring differs. E.g. Where China is heavily investing in IoT-based environmental monitoring networks, in the US, it seems we see a retreat from the government in this sector. To get an idea of the scale, consider what the Chinese government is currently doing, such as initiating IoT environmental monitoring programs like their Blue Sky program for Air Quality.

- Agriculture: Low-cost and easy-to-deploy IoT farming tools for the hundreds of millions of small-scale farmers in low-coverage areas, to support yield growth and food security through precision farming and monitoring weather and soil conditions.

- Other Uses: A myriad of applications for SMEs and even personal off-grid IoT devices are expanding the ecosystem in new and innovative ways as soon as satellite IoT applications' costs are down.

Customer Adoption

In 2025, large corporations continue to dominate with a nearly 80% market share, adopting SatIoT for cost control, resilience, and global operations. Customer adoption is strongly related to company size, with Small and Medium Enterprises (SMEs) currently lagging behind due to the cost and complexity of satellite IoT applications. Falling device and connectivity prices, along with standardised plug-and-play services, are expected to unlock mass-market adoption by 2030.

By then, SatIoT will transition from a niche to a core Industry 4.0 infrastructure, functioning as the global 4IR “nervous system” alongside terrestrial networks.

The Operators

At the supply side of the satellite IoT market we see that incumbent operators like Inmarsat, Iridium, Orbcomm, Globalstar and Echostar have 80% market share.

These players leverage legacy infrastructure, with reliable satellite networks and services, global coverage, global landing rights and frequency rights, global distribution and support networks have strong client bases. They serve established markets like defence and security, maritime, transport and logistics and the utility and energy market, most of them in large corporations from the US that require reliable and stable connectivity. The high value of their SatIoT applications justifies premium pricing.

Over the last five years, a next generation of satellite operators has been under development, working with a variety of technical innovations. Currently, more than 45 satellite constellations are under development.

CubeSat-based operators like Astrocast, Kineis and Myriota in 2025 have (major parts of) their constellations in space, often using dedicated frequency bands. These Low Power Global Area Network operators have launched their commercial services and are looking to scale.

HySky is a promising piggyback system that provides Ku/Ka band-based services from GEO satellites, and later also from LEO. Lower Ku/Ka bandwidth prices, compared to the L/S band operators, allow them to provide a wider range of satellite IoT services including voice and mid-band (150 kbps) data services.

Another group of operators use a standards-based approach, the 3GPP Non Terrestrial Network (NTN) or satellite LoraWan, offering hybrid terrestrial/satellite services.

Satellite operators developing or deploying services based on 3GPP standards include Sateliot and Skylo, and also Iridium’s Project Stardust and Eutelsat’s IRIS² via OneWeb.

Other operators like Lacuna, Fossa, Echostar Mobile and Challenger 1 have a satellite LoRaWAN approach.

They all aim to bring direct-to-satellite connectivity to the mass market—unlocking billions of potential devices. Dreams, sweet dreams.

Driving costs down is also the goal of picosat-based operators like Hydra Space, HelloSpace and Apogeo that are using VHF or UHF bands and the “free” (but contended) ISM band to provide their services. These system are still very much under development, and we have to see what service quality can be achieved in these bands, depending on the gods of interference.

An interesting approach also comes form Hubble Space, a system for tracking that works based on innovative Bluetooth connectivity to space.

We see a wide variety of next-gen operators that have one thing in common: their strategy centres driving down satellite IoT connectivity costs with easy to deploy end-to-end solutions with low-cost terminals, hybrid terrestrial / satellite networks. Their goal is making satellite IoT affordable and applicable for SMEs and consumers.

While the incumbent operators are growing their networks and customer base, and the LPGAN operators are looking to scale their commercial services, the supply side of the satellite IoT market is buzzing with dozens of next-gen operators each with their secret sauce using different orbits, satellite size, frequency bands and protocols. We will see in future how this works out.

The Scaling Phase of Satellite IoT

To get an idea of the dynamics in the next 5 years, we will have a look at some major issues the satellite IoT industry is facing.

"...We see a wide variety of next-gen operators that have one thing in common: their strategy centres driving down satellite IoT connectivity costs with easy to deploy end-to-end solutions with low-cost terminals, hybrid terrestrial / satellite networks. Their goal is making satellite IoT affordable and applicable for SMEs and consumers..."

Costs

Falling hardware and connectivity costs due to technological advancements and hybrid network strategies will help to drive down the costs of satellite IoT.

Where the high value of satellite IoT application for existing market segments justifies the premium pricing from incumbent operators, affordability remains a barrier in new cost-sensitive markets like environmental monitoring and agriculture.

Connectivity is only a small part of the total cost for a customer: application development, including sensor choice, edge computing, application data processing and user interface, as well as installation and customer support, are the main cost elements. This means cost-effective application development of end-to-end solutions and easy-to-install equipment as the key to driving down costs.

Only then will the existing market segments extend to new governmental, corporate, SME and even consumer markets.

Distribution Networks

Where incumbent operators had years to develop their global sales and distribution network with sensor partners, system integrators and service providers, for the next-gen operators, this is a main challenge that is going to take time and effort.

Standardization

Proprietary protocols complicate interoperability of satellite IoT network, that leads to operator lock up. In a time where we see a whole range of different satellite IoT networks each having it’s own pro’s and con’s for specific applications (or locations) this is not desirable as is can lead to sub-optimal network use.

Standardisation using terrestrial protocols is an effort to minimise this, but looking at the long life cycle of the incumbent (proprietary) IoT satellite constellations, we will be stuck with multiple protocols for the next decades. The use of Multi-IoT network devices, such as the M2sat IoT Communicator, is another way to address this issue.

Integration Complexity – SMEs face challenges in deploying Satellite IoT in their applications due to a lack of necessary technical expertise. It starts with the fact that they have to choose the proper satellite IoT network. Keep in mind, however, connectivity is only a small part of the full IoT solution. Knowledge of the fast-moving sensor, edge and data processing and UI industry (this is the 4IR!) is required to develop easy-to-use satellite IoT solutions.

Complexity, in particular, is a challenge for new players. Some operators, even from the latest generation, charge five-figure amounts for application and integration support, clearly targeting the corporate market only. However, incumbent satellite operators hold a strong position there and will defend it.

The establishment of a global ecosystem with system integrators and service providers is required, however, to create a breakthrough in the SME market.

Market Perception: Satellite IoT still carries the “too expensive, too complex” image, and the fact is that this is still true. Customer education is essential, not just to convince them via marketing that satellite IoT is simple and not expensive, but also to educate them on how to build end-to-end satellite IoT applications cost-effectively. M2sat IoT is doing that with its SatIoT application development program.

As part of the 4IR, satellite IoT applications are combining application knowledge with a whole set of sensor, connectivity and data processing technologies that so far are only dealt with in education silo’s. As long as this is the case, the perception of being too expensive and too complex will remain.

---------------------------

Hub Urlings was one of the pioneers of Satellite M2M/IoT as Product Manager of Inmarsat-C at the famous KPN Station 12. This "small data" satellite service's success, global coverage, and reliability made Inm-C the service of choice for many applications: from sending messages to truck fleet management to pipeline monitoring and bringing back data from all types of sensors. Now, 25 years later, he is still involved in developing a new generation of Satellite-IoT applications. In 2022, he founded SatIoTlab.com as a research, education, and co-creation platform for global satellite IoT applications.

Hub Urlings was one of the pioneers of Satellite M2M/IoT as Product Manager of Inmarsat-C at the famous KPN Station 12. This "small data" satellite service's success, global coverage, and reliability made Inm-C the service of choice for many applications: from sending messages to truck fleet management to pipeline monitoring and bringing back data from all types of sensors. Now, 25 years later, he is still involved in developing a new generation of Satellite-IoT applications. In 2022, he founded SatIoTlab.com as a research, education, and co-creation platform for global satellite IoT applications.