by Bruce Elbert

You can’t get into space without investment, and as the adage goes, you can’t make money if you don’t spend money. But first you need an idea or vision of what space can do for you and ultimately for a market. We got here through decades of innovation that put satellites in orbit, sent missions into space to the Moon and beyond, and found ways to use these for a variety of applications of value to mankind. The particular mix changes from time to time and today we see that LEO broadband and D2D have permanently changed satellite communications as a medium and a business. The rest of space is involved with earth observation, science and exploration. But some have suggested space commerce as a new way to make a buck off planet, so to speak.

All of this presents many new ways to enter the space economy and the money follows what is attractive and shows potential to be monetized through sales to various parties. I remember how Hughes Aircraft organized itself in the 1970s to engage in various segments of the space industry as it existed then. There were government programs in the defense domain since that customer needed competent technical resources. Then we had that innovative team led by Dr. Harold Rosen that established a commercial business that continues to this day. They drew technology and scientists from the governmental sector that was ahead of them. NASA was engaged in space development and Hughes garnered two important programs: Surveyor, which soft landed robotic spacecraft on the Moon ahead of the manned Apollo program, and Pioneer Venus that orbited a satellite around Venus and sent probes into the atmosphere and onto the surface of that planet. Weather satellites, also GEO, joined the product line since the government had taken a leadership role. In the 1980s and 1990s, Hughes went into the services segment by launching its own GEO satellites for TV and data services. All of that employed thousands of engineers and technicians as well as support personnel, and earned the owners good profits that established a valuation in the billions of dollars for the combined venture.

The non-GEO segment of satellite communications appeared in the 1990s in the form of Iridium and GlobalStar to provide a kind of personal communications service to handheld phones (called Direct-to-Device (D2D) today) using the L and S band frequency range, but both ventures went bankrupt so investors lost out. However, new parties came in after the debts were written off to transfer these systems to more viable niche applications, including serving government customers in the US and around the world. And despite the failure of Teledesic and Skybridge in the early 2000s, we now finally have deployed the broadband LEO systems such as Starlink that take over much of satellite communications. From here, it looks like more of the same in terms of services from LEO to all platforms and for interactive communications in nearly any form imaginable.

All of this is pretty mundane compared to some who see space commerce as being like what we saw in the mid-1800s with the gold rush out in the western United States. Some really huge mines appeared, like the Homestake mine in South Dakota that contributed to the overall economic development of the country. Are there minerals or other resources out in space that can be mined and delivered back home? Or should that mining produce material for further extraterrestrial development on Mars and beyond? It’s like science fiction but here we are talking about activity that can be financed perhaps privately with the product hopefully monetized for the benefit of investors. In other words, can we make money out in space? Or is this destined to be a repeat of the late 1990s, when the technology was developed to deploy LEO satellite communications constellations, but the hoped-for commercial market did not materialize for these systems.

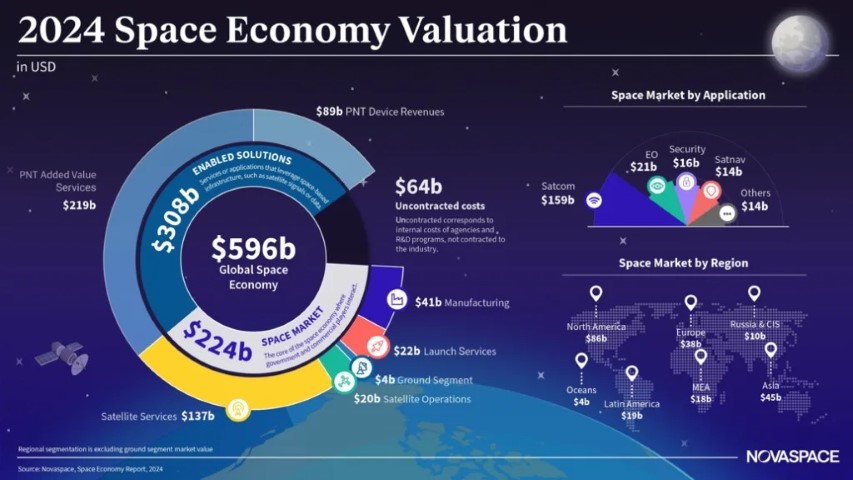

"...Investors seek opportunities based on innovative technology and the strength of the team. But customers compare cost/effective benefits and thereby decide who wins the space race..."

There is an interesting example from the 1970s that combines a commercial business concept with a seemingly unrelated government activity. A ship with the name of the Glomar Explorer was constructed by a company called Global Marine whose announced purpose was to mine manganese nodules under the ocean. That company was headquartered in the office building in El Segundo, California, where I happened to work. The ship was completed in 1973 and had some interesting technology, including a giant claw made by Kaiser Steel. Hughes Tool was the investor and developer and it was owned by Howard Hughes. There was great interest because it seemed as far out as mining the Moon but perhaps a bit more practical since it would use naval technology, well established over hundreds of years. However, it turned out that this was another government contract with the purpose of raising a sunken Soviet submarine, which Hughes technologists actually did.

Mining is a fundamental business as long as you know what you are mining, how much ore is available, and the concentration of whatever valuable mineral is contained therein. Gold is an excellent example because its quantity is limited, it has value, and it’s quite concentrated as far as that value is concerned. There are costs in dealing with something like gold mining, and the story is well understood here on earth. You can pencil this out if you have the information, including the cost of recovery, processing and transfer. But as far as space is concerned, there are many unknowns that put this more in the domain of scientific research than economic development. The 2009 movie, Moon, gave us a fascinating picture of mining of Helium-3 on the far side of the Moon, where this rare isotope was used for a powerful energy source on earth. It’s a wild ride but the construct of using robotic excavators to produce a relatively compact substance might demonstrate the principle.

Closer to earth, the rescue of two astronauts on the US International Space Station (ISS) in March of 2025 by the SpaceX Dragon capsule suggests an ongoing need for a kind of 9-1-1 service in space. The idea is that some organization (company or government agency) maintains a launch vehicle and capsule on the ready to be used to perform this kind of mission. It has some similarity to GEO mission extension provided by Northrup Grumman that has already been used and has a reasonable future as current GEO spacecraft reach end of life.

|

The TV series, Constellation, which streams on Apple TV+, points to the same problem where one astronaut was left on board ISS after the entire mission encountered the classic “Houston, we have a problem” kind of major onboard failure. Apple’s producers did a great job visually including their great sets, animation and simulating weightlessness. They properly employ an orbit period of 90 minutes and the need to store energy during the 45 minute eclipse that blocks the sun from the solar panels. I enjoyed how that single astronaut figured out that she needed to replace the failed batteries used to store energy during sunlight. But the bigger issue is how we can rescue people when stranded. It took nearly a year until the SpaceX Dragon capsule was engaged to return the stranded pair back to earth. Is this a business model to have the rescue ready, like a kind of 9-1-1 emergency response? Again, it’s straightforward to estimate the cost of having a rocket and capsule ready, the way SpaceX already accomplished. The cost of having a crew available is another knowable item. But the bigger question is how to fund this venture and how to charge a customer for the availability and use. It was in the business plan for GEO satellites of a startup called AssureSat, but this venture failed to move past funding and early development.

Which brings me to how business people view the government as their customer. It’s the age old system of supplying war materiel under contract, lucrative ever since President Abraham Lincoln bought the first steam ships during the Civil War. Whether it’s ships on the water or ships in space, the game is the same. When I was on my job search in 1969 at the end of my military service, I was interviewed at Texas Instruments for a position as a communications systems engineer. One of the more impressive managers I met talked about what he called the “Space Biz”. He gave the example of Ling Temco Vaught (LTV), a big government contractor based in Texas. He spoke about Jimmy Ling, the electrical contractor who created that massive technology conglomerate. I hadn’t considered space as a career and I didn’t end up at TI; however, I did take a position as a member of the technical staff at COMSAT Laboratories. In those days, space business became established heavily in government contracting which means you had to know how to be aware of government needs and how to convince the government of the strength of the offer. Lockheed, Hughes, TRW, Grumman and Boeing figured this all out and effectively partnered with the government to supply whatever capability was called for.

Space was the domain of these large companies as well as a few others in Europe and Asia. We can talk about the degree of vertical integration, that is, how much of a given system is made by this contractor as opposed to a supply chain of numerous other companies. In fact, contributing to the supply chain is a viable business for those who have a critical technical ability and can deliver it at a competitive price. Companies like L3 Communications, now merged with Harris, Sunstrand, Honeywell, CPI and Ball Aerospace have a long record of meeting the needs of these prime contractors. But new players have appeared in the last ten years that receive venture financing because of the promise of the space economy.

Based on past experience, any new device and supplier must first undergo rigorous space qualification, following something akin to NASA’s Technology Readiness Level (TRL) certification process. This considers product quality and space worthiness and manufacturer dependability.

Further, the prime contractor must itself qualify the product for application in its spacecraft and mission. Back in the 1970s, one of the named primes approached Intelsat with a new vehicle concept, claiming it was qualified based on a partial test model in a lab environment. I am familiar with lab testing because Hughes subsequently assembled a structure with attitude control elements that demonstrated the principles needed for a three-axis attitude control design. But, it was not a full engineering model or prototype spacecraft such as needed for a real program for a customer with its own operation.

Let’s take a look at some early space technology ventures that can support the supply chain of prime contractors. Several of the following produce launch vehicles of various sizes and small spacecraft for a variety of missions. Also given are suppliers of key components for spacecraft in the bus and payload.

Launch Vehicles

- Rocket Lab: Not only produces its Electron and Neutron rockets but also manufactures its Photon satellite platform.

- Astra: Develops its own rockets and electric propulsion systems for satellites.

- Blue Origin: Creates reusable launch vehicles like New Shepard and New Glenn, along with its BE-4 rocket engine.

- Relativity Space: Uses 3D printing to create its Terran rockets and offers a platform for designing, building, and flying them.

- Firefly Aerospace: Manufactures its own Alpha and Beta orbital rockets.

- York Space Systems: Provides standardized satellite bus platforms for various missions.

Propulsion Systems

- Accion Systems: Creates electrospray propulsion systems for small satellites based on technology developed at MIT.

- Applied Ion Systems LLC: Aims to lower the cost of electric propulsion systems for nanosatellites and picosatellites.

- Dawn Aerospace: Manufactures non-toxic, electric, and propellant-based propulsion for a range of aerospace applications.

- Exotrail: Provides electric propulsion systems and mission design software for smallsats.

Spacecraft Bus

- Solestrial – manufactures specialized solar panels

- SOLARMEMS – manufactures sun sensors and other sensing devices

- Redwire – manufactures rollout solar panels, structure and other vehicle systems

- Blue Canyon Technologies - supplies integrated Attitude Determination and Control Systems (ADCS), including its own star trackers and a new line of reaction wheels for larger spacecraft, acquired by Raytheon in 2020.

RF Communications Payload

- Quorvo: Solid state microwave transistors.

- Narda-MITEQ – long time supplier of microwave devices

- Erzia – solid state microwave power amplifiers

- MIRAD – passive microwave devices

- Tendeg – deployable reflector

- Space Optical Terminals

- MBRYONICS, Ireland – StarCom product line for proliferated systems

- TNO, Netherlands – Raytheon funding, deep space terminal

- Mynaric, Germany (US and Canada) – CONDOR terminal, flight proven

- CACI - Crossbeam tested on Mandrake II

- TESAT, Germany – very experienced in GEO, SCOT products for LEO

- Skyloom, US – Japanese funding, potential EO constellation use

- SpaceX – offering its LEO ISL terminals.

The new space paradigm has produced several prime contractors currently smaller than those who lead the government sector. SpaceX surely is no longer small in this contact and is a powerful force in terms of rockets and small satellites. Others like York and Astroscale have garnered government contracts, and still others like Astranis and SWISSto 2 are up and coming in the commercial GEO sector. Vertical integration as a strategy comes and goes, and today it’s a little like that Michael J. Fox movie, Back to the Future, which first played forty years ago. SpaceX has done an excellent job supplying itself with both the complex and the basic, and newcomers like EO provider Planet Labs have exploited this strategy for reasons of confidence, control and perhaps schedule assurance. They reached a quarter of a billion dollars of revenue after just 14 years operating lots of microsats with growing capabilities in terms of photographic and spectral scanning data delivery.

Investors seek opportunities based on innovative technology and the strength of the team. But customers compare cost/effective benefits and thereby decide who wins the space race. In 2000, many of the dot-coms got funded and went public even without revenue from the identified product or service. RateXchange, for example, began as a telephone equipment installer with revenue from commercial customers, but subsequently merged with a public shell corporation to create the first bandwidth exchange on the Internet. Interestingly, there was no underlying technology or team, just an unrelated revenue stream and a catchy name at the peak of the bubble. The presumption of value in bandwidth trading was fake, made worse by the collapse of demand for bandwidth post 2000.

More to the point, some new technology players are getting traction in the government sector, owing to difficult mission demands and hoped-for commercial-like program performance. It is possible that aggressive new firms can produce results as good or possibly better than the status quo. We have large missile defense shields, lunar exploration and even AI in space all the rage. Ideally, you want a technological solution that plays across multiple domains, or you want to have a unique solution for specific but certain applications, probably based on high quality and high price. Both the buyer and seller may be new to this game, in which case caveat emptor. By this I mean that the buyer needs comparable technology and management knowledge and experience when performing the due diligence on supplier and product. Contracts are intended to assure results but there are recent cases where the new supplier discovers they overpromised and underperformed, leaving the buyer in the awful position of either finding an alternative or sticking with the current source and even helping them meet their obligations.

The space game is crowded by new and old suppliers and customers, and the technology is moving quickly. Still, I wouldn’t be surprised to see an old-line major gain prominence through its experience and resources. Back during the Apollo program, Boeing was responsible for only the giant first state of the Saturn V rocket while others supplied the rest of the vehicle and payloads. NASA retained responsibility for integration and verification. But the fire on Apollo 1 in 1967 that killed three astronauts lead to a change where Boeing was given responsibility for overall systems engineering, vehicle integration, and mission support. The criticality of Boeing’s increased role was demonstrated by the complete success of this part of Saturn throughout all of the launches.

A member of the investment community who spoke at the recent World Space economic meeting in Paris stated that any new venture in space should show a revenue stream. This means that the company should be on track to profitability and valuation. Any new space idea must pass this test. Those that do, like SpaceX, can end up leaders in the space economy of the future.

--------------------

Bruce Elbert is a Contributing Editor of the Satellite Executive Briefing magazine the Founder and President of Application Technology Strategy LLC.(www.applicationstrategy.com) He is a satellite industry expert, communications engineer, project leader and consultant with over 50 years experience in communications and space-based systems in the public and private sectors. He can be reached at: bruce@applicationstrategy.com

Bruce Elbert is a Contributing Editor of the Satellite Executive Briefing magazine the Founder and President of Application Technology Strategy LLC.(www.applicationstrategy.com) He is a satellite industry expert, communications engineer, project leader and consultant with over 50 years experience in communications and space-based systems in the public and private sectors. He can be reached at: bruce@applicationstrategy.com