by Vivek Prasad

Non-GEO constellation players have transformed the satellite communication (satcom) industry in the past five years. Leading this transformation is Starlink, which has set new benchmarks in satellite deployment speed, capacity influx, and customer acquisition. Other players like Amazon’s Kuiper, Eutelsat’s OneWeb, Telesat’s Lightspeed and SES’s mPower continue to reinforce the viability and advantages of Non-GEO solutions. As nations increasingly recognize the benefits, such as scalable bandwidth and reduced cost per Mbps, there is a growing shift toward developing sovereign constellations. These national initiatives are driven by the urgent need for secure communications, digital autonomy, and strategic resilience in response to shifting geopolitical landscapes and rapid technological progress.

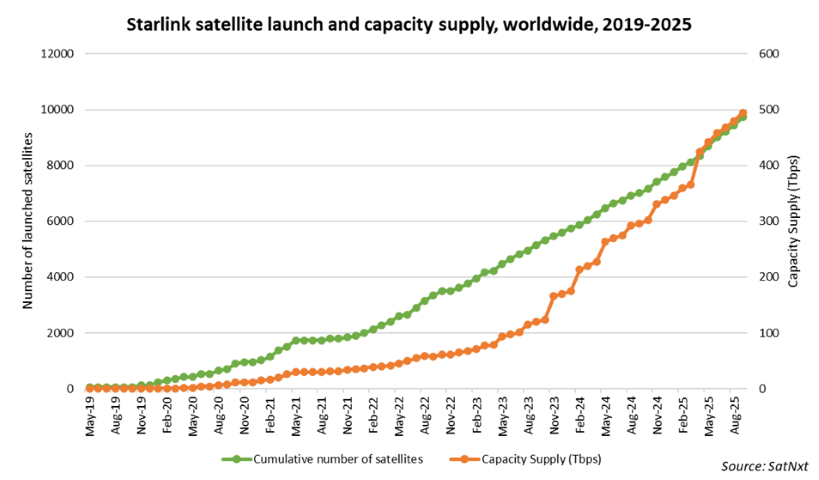

The Starlink impact

The unprecedented growth of Starlink has fundamentally reshaped the satellite communications landscape. In just five years, the company has launched over 10,000 satellites, adding approximately 500 Tbps of satellite capacity in orbit. Alongside its rapid deployment pace, Starlink has progressively upgraded its satellites from versions V0.9 to V1, V1.5, and V2 Mini, with each iteration enhancing per-satellite throughput. In its upcoming version, the company aims to achieve a throughput of 1 Tbps per satellite. While Starlink demonstrates clear dominance in the satellite broadband market, this has also raised concerns about national autonomy. Notably, Starlink’s broadband service has been utilized in high-stakes environments, such as wartime communications in Ukraine. Amazon’s Kuiper is also rapidly developing the mega-constellation to compete directly with Starlink, leveraging its retail ecosystem and AWS infrastructure. The Chinese government-backed Guowang constellation aims to expand China’s digital footprint and influence, particularly in the Belt and Road Initiative partner countries. Considering these advancements, nations face growing concerns over foreign player service suspension, data interception, and traffic prioritization, especially during geopolitical tensions. Another concern is the orbital slot race, where spectrum congestion and orbital crowding may restrict access for late entrants. These advancements and associated concerns have led nations to increasingly prioritize the development of sovereign satellite constellations.

Indicators signalling the global rise of sovereign constellation

A major indicator of the global momentum toward sovereign satellite constellations is the European Union’s IRIS2 program. This initiative reflects Europe's strategic intent to reduce reliance on non-European satellite connectivity networks, by deploying a multi-orbit constellation of 290 satellites by 2030. The program is led by the SpaceRISE consortium with incumbent satellite operators, SES, Eutelsat, and Hispasat. The consortium has extensive network of partners including Airbus Defence and Space, Deutsche Telekom, OHB, Orange, OHB, Hisdesat, Telespazio, Thales Alenia Space, and Thales SIX. The focus will be to provide secure communication to EU member states, covering government, enterprise, mobility and broadband applications.

India is actively evaluating the development of a sovereign LEO satellite constellation to address the country’s broadband connectivity needs. Various government departments are assessing both civil and strategic requirements to determine the viability of this initiative. The current consideration involves deploying ~140 satellites to meet immediate bandwidth demands, with a strong focus on supporting government services and enabling digital inclusion across underserved regions. Notably, India has already granted permission to foreign operators such as Starlink and OneWeb to offer satellite broadband services within its borders. This move underscores the urgency of establishing a sovereign alternative to ensure long-term digital autonomy, secure communications infrastructure, and strategic resilience in an increasingly contested orbital environment.

Australia has announced a consortium led by Optus to develop LEO satellites within the country. The initial developmental satellite will carry both earth observation and connectivity payloads. The broader vision is to build national LEO capabilities and potentially scale the technology into a sovereign satellite constellation.

Other countries likely to pursue sovereign satellite constellations in the coming years include the UAE with Space42, and Saudi Arabia. Both nations are aiming to secure national digital sovereignty and accelerate the development of their domestic space ecosystems. Their strategies are expected to range from building indigenous satellite constellations to forming strategic collaborations with global players.

The future of sovereign constellations

The race for control over sovereign satellite constellation infrastructure is intensifying, driving increased investments from governments and national agencies that will significantly benefit the broader space industry ecosystem. While the strategic rationale for sovereign constellations is compelling, decision-makers must carefully evaluate the economic sustainability of such initiatives.

Non-GEO satellite constellations are inherently capital-intensive, with shorter satellite lifecycles and rapid technology turnover. Designed for global coverage, these systems face fundamental inefficiencies when restricted to serving a single nation, leading to underutilised capacity and potentially unsustainable operations. To mitigate this, nations must develop robust strategies to commercialise capacity on a global scale and account for existing and emerging competition. Ultimately, true and sustainable sovereignty in the Non-GEO connectivity domain will depend on achieving a balanced approach, one that harmonises autonomy with strategic partnerships, secure networks with commercial openness, and national investment with cooperative efficiency.

---------

Vivek Prasad is the Founder and Director of SatNxt (www.satnxt.com). He began his career as scientist at the Indian Space Research Organization (ISRO) in 2010, contributing to the design and integration of seven earth observation and scientific satellites, including SARAL, ASTROSAT, and INS-1A & 1B. After seven years at ISRO, he joined Frost & Sullivan in 2017, where he expanded Space Industry Practice and earned the President’s Club Executive Award. He later served as Head of Satellite Capacity Programs at Analysys Mason (formerly NSR), leading global research and advisory projects across satellite constellations, satcom wholesale, enterprise connectivity, consumer broadband, maritime, and cloud markets. With 15 years of experience spanning satellite missions, market intelligence, and strategic consulting, Mr. Prasad has authored over 60 industry reports and client engagements. At SatNxt, he leads market intelligence and consulting initiatives across the entire space industry value chain, transforming complex satellite market data into actionable insights that drive confident, high-impact decisions. He can be reached at: vivek@satnxt.com

Vivek Prasad is the Founder and Director of SatNxt (www.satnxt.com). He began his career as scientist at the Indian Space Research Organization (ISRO) in 2010, contributing to the design and integration of seven earth observation and scientific satellites, including SARAL, ASTROSAT, and INS-1A & 1B. After seven years at ISRO, he joined Frost & Sullivan in 2017, where he expanded Space Industry Practice and earned the President’s Club Executive Award. He later served as Head of Satellite Capacity Programs at Analysys Mason (formerly NSR), leading global research and advisory projects across satellite constellations, satcom wholesale, enterprise connectivity, consumer broadband, maritime, and cloud markets. With 15 years of experience spanning satellite missions, market intelligence, and strategic consulting, Mr. Prasad has authored over 60 industry reports and client engagements. At SatNxt, he leads market intelligence and consulting initiatives across the entire space industry value chain, transforming complex satellite market data into actionable insights that drive confident, high-impact decisions. He can be reached at: vivek@satnxt.com